Q1 2026: what recent records really say about the top end of the collector car market

Q1 2026 confirmed the strength of the top end of the collector car market. But behind the records, the key signal lies elsewhere: the market is becoming more polarised. Value is concentrating around the best specified, best documented and most desirable examples.

The first quarter of 2026 delivered a sequence of results strong enough to draw attention well beyond the usual circle of collectors. Records were set in rapid succession, sell-through rates remained high on the most important lots, and international participation confirmed the widening of the buyer pool at the very top of the market.

It is tempting to read this as proof of a broad-based market upswing. That would be incomplete.

What the early results actually indicate is not a uniform rise across the market. They point instead to a sharper form of polarisation, favouring cars that combine several qualities that have now become decisive: rarity of specification, strong provenance, impeccable documentation, coherent condition, low mileage where relevant, and deep generational desirability.

In other words, the market is no longer paying indiscriminately for a model. It is paying ever more for a specific car.

A sequence of sales that signals a change in scale

Kissimmee, Arizona, Paris, Miami and then Amelia Island traced the same pattern within a matter of weeks: more capital, more competition for the best lots, and a clear concentration of the most spectacular results at the very top of the pyramid.

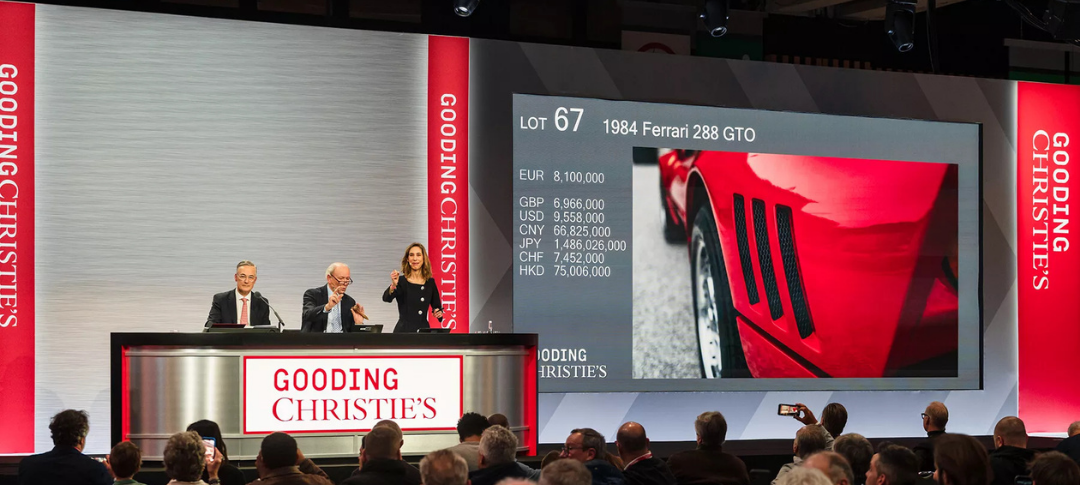

A few reference points are enough to measure the scale of the shift. Mecum Kissimmee generated $441m in total sales, nearly double its 2025 figure, with 54 lots above $1m. At the same time, Ferrari’s halo models — the 288 GTO, F40, F50, Enzo and LaFerrari — all set new auction records within the space of a few weeks. At Amelia Island, Broad Arrow delivered its largest sale in 31 years, achieving $111m with a 92% sell-through rate, driven by more than 1,000 bidders from 23 countries. The sell-through rate for lots estimated above $1m reached 90%.

On a rolling 12-month basis, auction sales of cars above $1m crossed the $1bn threshold for the first time. Yet the most useful reading is not purely quantitative. Yes, aggregate values are high. Yes, records are multiplying. But the most significant point lies elsewhere: the market is executing more effectively on the most desirable lots, while the rest of the supply remains subject to far greater selectivity.

That distinction matters. It suggests a market that is maturing. In a young or speculative market, rising prices tend to spread broadly. In a more mature market, capital becomes exacting. It no longer rewards mere association with a name or lineage; it rewards genuine rarity, coherence of specification, quality of preservation and clarity of documentation.

Three drivers now shape price formation

1. Specification is no longer a detail. It has become a multiplier.

The first driver is specification. The gap between two examples of the same model can now be considerable when one benefits from a rare colour, special-order factory configuration, desirable options or particularly strong aesthetic coherence.

The market is becoming less willing to pay for the ordinary and more willing to pay for the clearly exceptional. This shift is not anecdotal. It changes the way value must be analysed. For years, many buyers thought primarily in terms of model and only secondarily in terms of detailed specification. That approach is no longer sufficient.

A rare car is no longer simply a little better than another. In some cases, it effectively belongs to a distinct sub-market of its own.

The clearest illustration of the quarter came from the two Porsche Carrera GTs sold on the same weekend at Amelia Island: one sold for $6.7m at Broad Arrow in Paint to Sample Gulf Blue, one of only two produced in that colour; the other sold for $3.1m at Gooding in GT Silver Metallic. The model was the same. The specification was not. In very concrete terms, the market reminded everyone that an average value for the model never applies to a real car.

The implication is straightforward: any aggregated reading along the lines of “this model is now worth X” has become dangerous. The real question is not what the model is worth. The real question is what this particular car is worth, in this specification, with this history and in this condition.

2. Provenance and documentation have once again become assets in their own right

The second driver is provenance. The market continues to reward what cannot be recreated: long-term single ownership, continuity of possession, a clear history, factory certifications, complete documentation, original accessories and clear maintenance records with no grey areas.

That premium can sometimes outweigh even strict cosmetic correctness. A car may show an imperfection on one point and still outperform thanks to intact mechanical authenticity, remarkable continuity of ownership, or an exceptionally strong supporting file.

The Lamborghini Miura P400 SV sold for $6.605m at Amelia Island illustrates this logic perfectly. Repainted in the 1970s and therefore no longer in its original colour, it nevertheless set a model record thanks to more than half a century of single ownership, intact matching numbers, desirable options and a remarkable dossier. In this case, continuity of ownership mattered more than strict aesthetic conformity.

This reflects an important evolution in the market. Value is no longer created only at the moment of purchase or sale. It is created throughout the holding period. The care devoted to preservation, traceability, work performed and their documentation becomes a direct driver of future value.

For collectors, this means an exceptional automobile can no longer be managed as a static object. For investors, it means that performance depends in part on the discipline of ownership.

3. Generational transition continues to support analogue cars

The third driver is demographic. Generation X and millennials continue to direct a growing share of their capital towards the automobiles that shaped their imagination: analogue supercars from the 1990s and 2000s, cult models discovered in specialist magazines, on track, or through the visual and video-game culture of the period.

Demand is concentrating first on cars that combine three attributes that have become rare together: a manual gearbox or a deeply mechanical driving experience, a naturally aspirated engine, and an absence of intrusive electronic mediation.

This trend extends beyond the most established blue-chip references. It is also reaching certain niche manufacturers and several Japanese and German icons long regarded as specialist markets. When generational memory meets structurally limited supply, a market can change regime quickly.

The Nissan NISMO 400R sold for $918,000 at Broad Arrow’s Amelia Island sale is a telling signal in this respect. So too is the unusually high number of RUFs brought to market since the start of 2026 — no fewer than eight cars. Models once confined to cult status among a generation raised on the Gran Turismo video-game culture of the 1990s are now entering the realm of recognised collector assets. This shift should not be overstated, but it can no longer be ignored.

That said, the underlying trend must be distinguished from its possible excesses. Not every so-called analogue car is destined to become a blue-chip asset. Depth of demand, genuine rarity, the quality of available cars and future liquidity remain decisive.

The real issue: a two-speed market

Behind the records, the quarter’s main signal is therefore polarisation.

The top of the market continues to absorb capital with remarkable efficiency. By contrast, a large part of the mid-market is operating in a far more demanding environment. Buyers there are more cautious, more selective and less willing to pay a premium for cars that are merely correct.

This polarisation can be read in several ways. First, liquidity is concentrating on cars that meet several quality criteria at once. Second, the dispersion between two particular car of the same model is widening. Third, the economics of restoration are becoming tighter in many segments: rising specialist labour costs, parts inflation and stricter decisions on whether a project still makes financial sense.

The market is therefore increasingly favouring two very different profiles, both of them easily legible: either the no-compromise turnkey example in outstanding condition, or the deeply original particular car whose patina or preservation tells something irreplaceable. Between the two, the middle ground is narrowing.

What this changes in the way the market must be read

The most important consequence is methodological. It is becoming less and less relevant to comment on results through broad abstract categories. The the high-end collector car market is not simply more expensive than it used to be; it is more discriminating than it used to be.

This means that general indices, model-based comparisons or conclusions drawn too quickly from a single record are becoming less useful. They indicate a direction, but rarely provide a sufficient basis for decision-making.

To interpret the quarter correctly, two ideas must therefore be held together: yes, the top end of the market is very strong; no, that strength does not spread mechanically across everything else.

It is precisely within that gap that the most important analytical work now sits.

What to watch in the coming months

Three questions will determine whether the current regime is truly durable.

First, will these new price levels be validated across several consecutive sales rather than one particularly strong quarter?

Second, will the premium attached to rare specifications and impeccable dossiers continue to widen, further increasing the gap with cars that are simply good?

Third, will international participation and the growing institutionalisation of the very top end be sustained over time?

These signals still need to be confirmed through time. A market does not change regime on the strength of one quarter alone, however remarkable.

Conclusion

The beginning of 2026 does not point to a uniform rise in the exceptional automobile market. It reveals something more interesting: a market that is more mature, more selective and more demanding, in which value is concentrating in the best-specified, best-documented and most desirable cars.

In such an environment, analysis can no longer stop at model level. It must move down to the level of the individual car. That is now where price gaps are created, where genuine opportunities emerge and, symmetrically, where the most costly mistakes are made.

Sources and references

Mecum Auctions — Kissimmee 2026 Results

Broad Arrow Auctions — Amelia Auction 2026 Results

Gooding Christie’s — Amelia Island Auctions 2026 Results

Hagerty — market and auction data, 2025–2026

RM Sotheby’s — public auction results and market references, 2025–2026

Photo credits

Main picture: Gooding Christie’s

Do you have a project in this segment? We can deepen this analysis for your specific situation.

Contact us